Last month’s publication of the UK Government’s Reformed National Pricing Delivery Plan is an important step in the long-awaited evolution of electricity market reform. Alongside recent publications from Ofgem and NESO, many of the key building blocks needed for a more strategically planned system are emerging. But despite that progress, there remains a huge amount of confusion about how these different pieces fit together.

At the centre of that confusion is a more fundamental question: what actually constitutes a strategic plan for the electricity system?

In recent weeks I’ve heard people refer to the SSEP – the Strategic Spatial Energy Plan – as “the plan.” Given the name, that seems entirely reasonable. But to me, the SSEP is only one component of what we need if we want a genuine plan, capable of delivering directed change in the real world.

Historically, Great Britain’s electricity system has relied on markets to determine the location and timing of infrastructure investment, with network development following behind. Increasingly, however, the scale, pace and coordination required for decarbonisation means that the market approach is no longer sufficient on its own.

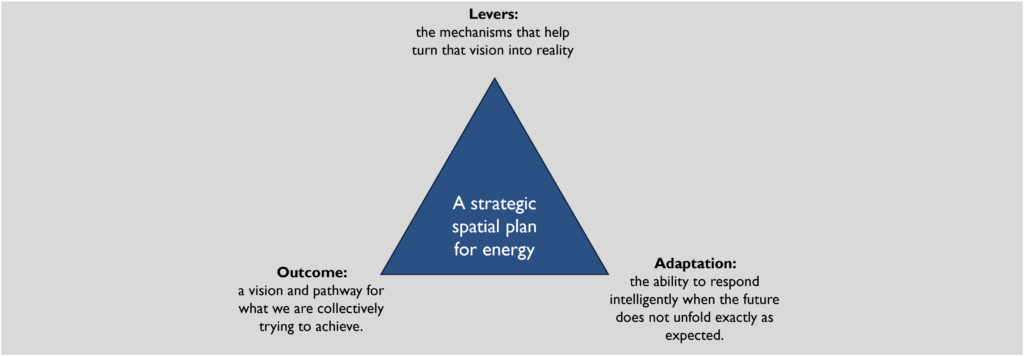

Rather, a growing degree of centralised strategic planning is needed. Such a plan needs three components:

- Outcome: a vision and pathway for what we are collectively trying to achieve.

- Levers: the mechanisms that help turn that vision into reality.

- Adaptation: the ability to respond intelligently when the future does not unfold exactly as expected.

The SSEP (despite its name) is only part of that plan. It represents the outcome – or more accurately, the pathway – because it will describe, to some degree or another, what we collectively want the future energy system to look like and how infrastructure might be spatially coordinated to get there.

Alongside that pathway sit the levers: processes, incentives and institutions that will collectively shape whether the pathway is delivered. Those levers sit across government, regulator, system operator, infrastructure developers, energy consumers and citizens. Much of that emerging framework is now being set out through the RNP Delivery Plan and associated reforms.

Finally, a credible strategic plan requires the ability to adapt. The future will not unfold exactly as expected. Technology costs may change. Supply chains may tighten. Demand growth may accelerate. Political priorities may evolve. Strategic planning therefore cannot simply be a static blueprint frozen in time. It needs mechanisms for adjustment, iteration and response. In some cases, adaptability may mean pulling harder on the existing levers if delivery falls behind expectations. In others it may mean adapting the pathway itself and allowing greater flexibility in the eventual mix and capacities of technologies deployed in different regions.

So, to me, the SSEP on its own is not “the plan.” Rather:

Strategic Plan for the GB system = SSEP + RNP Delivery Plan + Course Correction

The three components of a successful strategic energy system

Component 1: The Outcome

The SSEP is the outcome – or more accurately the pathway. NESO describes it as: “a GB-wide plan, mapping potential zonal locations, quantities and types of electricity and hydrogen generation and storage.”

In simple terms, it aims to set out how much of each technology type we might need, in which parts of the country, and at what point in the transition.

That pathway is being developed through a combination of approaches. At its core are optimisation models that seek to minimise the cost of delivering specified outcomes: electricity demand, carbon targets and security of supply. Layered on top are real-world constraints around land use, geography and infrastructure.

Importantly, the SSEP pathway is not trying to predict the future. Prediction is the wrong framing because we are collectively responsible for bringing that future about. We – government, regulator, system operator, developers, investors and citizens – have agency over what happens. The outcome is entirely dependent on us doing things.

The purpose of the SSEP pathway is therefore not to produce a perfectly accurate forecast of what the energy system will become. It is to coordinate investment and decision making under uncertainty and build broad consensus around the direction of travel. Ultimately, its role is to provide a shared vision that all stakeholders buy into.

Component 2: The levers

A pathway described in a report is, on its own, of limited use. We have had plenty of pathways before: Future Energy Scenarios, the CCC’s Balanced Pathway and various government scenarios, to name just a few.

The SSEP only really becomes a strategic plan when it is yoked to appropriate delivery levers.

Many of those levers are now emerging through the Reformed National Pricing (RNP) Delivery Plan. Government describes RNP as a “portfolio of interventions spanning the whole of the power sector,” including:

- reforming siting and investment incentives to support delivery of the SSEP;

- reducing network constraint costs; and

- improving system operability and efficiency.

There are other levers too: planning reform, consenting reform, connections reform, support mechanisms and operational market arrangements. The important point is that these are not separate from the plan. They are the mechanisms through which the pathway is either delivered or undermined.

Component 3: Adaptation and course correction

Strategic planning creates a new tension between the SSEP pathway and what we might loosely call “the market”. Historically, Great Britain largely allowed the market to determine the generation and flexibility mix, while the transmission network attempted to follow on ahead. To “follow on ahead” sounds like a contradiction, it means that network planning still relied on assumptions about what the market was going to build years into the future, and a hope that those assumptions would be sufficiently correct to justify the investment. It was a difficult challenge, and uncertainty – real or perceived – over what the market might do in the future was often used as a rationale for stepping back from network investments. As today’s constraint costs demonstrate, we did not always get the balance right.

Under the SSEP framework, the challenge changes but does not disappear. The best we can realistically hope for is alignment between the pathway and market conditions at the point the SSEP pathway is developed. From that moment onwards, reality will begin to diverge from the pathway: projects are delayed, technology costs shift, demand levels change and political priorities evolve.

That creates an important governance question: what do we do when outturn no longer matches the pathway?

At present, the main mechanism for that course correction is the proposed three-year SSEP cycle. If the first SSEP is published in late 2027, as currently expected, a second iteration would follow in 2030. That may prove sufficient. But whether it is depends partly on a much bigger question: how firmly do we actually intend to hold to the plan in the first place?

The authority of the plan versus the authority of the market

Broadly, there are two options to respond to deviations from what we expect: we can double down on the SSEP pathway and pull the levers harder to bring reality back towards the plan. Or we can adapt the pathway itself in response to changing conditions.

The first supports certainty for the system, meaning that there is a focus on realising the value that long term investments already underway, such as transmission build-out. The second supports flexibility, acknowledging that, as John Maynard Keynes famously said, “When the facts change, I change my mind. What do you do, sir?”

The entire rationale for strategic planning was that the existing market-led approach was no longer delivering coordinated outcomes. That suggests the plan itself must carry some authority. Not because it is guaranteed to be objectively “right”, but because coordination has value in its own right.

Take a simplified example. We might conclude there are two credible pathways to decarbonisation:

- Option 1: more floating offshore wind in Scotland and less fixed offshore wind in England;

- Option 2: or more fixed offshore wind in England and less floating offshore wind in Scotland.

Both pathways might ultimately work. And with hindsight, we may discover the alternative would have been cheaper. But strategic planning is partly about accepting that uncertainty and still choosing a direction.

The logic looks something like this:

- we think one option is likely to be better;

- we accept we may later discover we were wrong;

- but we won’t know whether we were wrong until several years time (if ever);

- therefore there is greater system value in choosing a pathway, our ‘best guess’ today, sticking to it, and coordinating around it.

That is ultimately an argument for giving the plan some authority over the market. But it is also a nuanced argument that needs to be balanced against the value that market signals can give us.

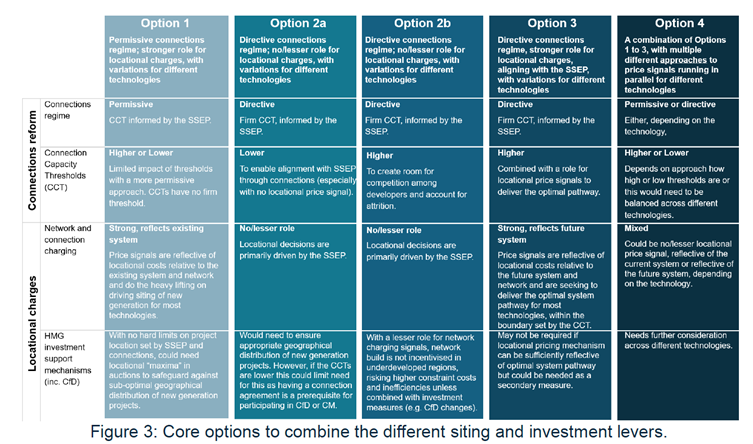

RNP siting and delivery levers: a spectrum of authority for the plan

The siting and investment options within the RNP Delivery Plan are, at their core, different answers to a fundamental question: how much authority should the SSEP pathway actually have?

The options include different roles for the connection regime, network charging and investment support mechanisms in shaping the locational distribution of technologies, in effect different roles in ‘delivering’ the SSEP pathway.

Broadly speaking then, the siting and investment options put forward in the RNP delivery plan can be thought of as a spectrum between stronger market authority and stronger plan authority.

Option 1 sits closest to the historic market-led approach. It allows connections to diverge more significantly from the SSEP pathway and continues to rely heavily on locational charging signals based on the existing network to “internalise” system costs into investment decisions. Support mechanism maxima may still place some limits on deployment in particular regions, but overall, the market retains substantial freedom to determine outcomes. If we adopt this approach, I think I would question whether it was really strategic planning at all.

At the other end of the spectrum, Option 2A represents a much stronger form of strategic coordination. Connections would follow the SSEP pathway much more closely, with the focus shifting toward ensuring that sufficient projects come forward to deliver the pathway and that those receiving connection offers are ultimately built. If we adopted this approach I would worry that we were not giving ourselves sufficient flexibility to deal with an uncertain future – we would be very dependent on making the specific set of choices we went with work perfectly.

Options 2B and 3 sit somewhere between those two extremes. They allow more projects to receive connection offers than are strictly required by the SSEP pathway, while still using available levers to steer the overall outcome back towards the plan over time. In effect, these models use plan authority to decide who gets to the table, but market authority to decide who ultimately wins the game.

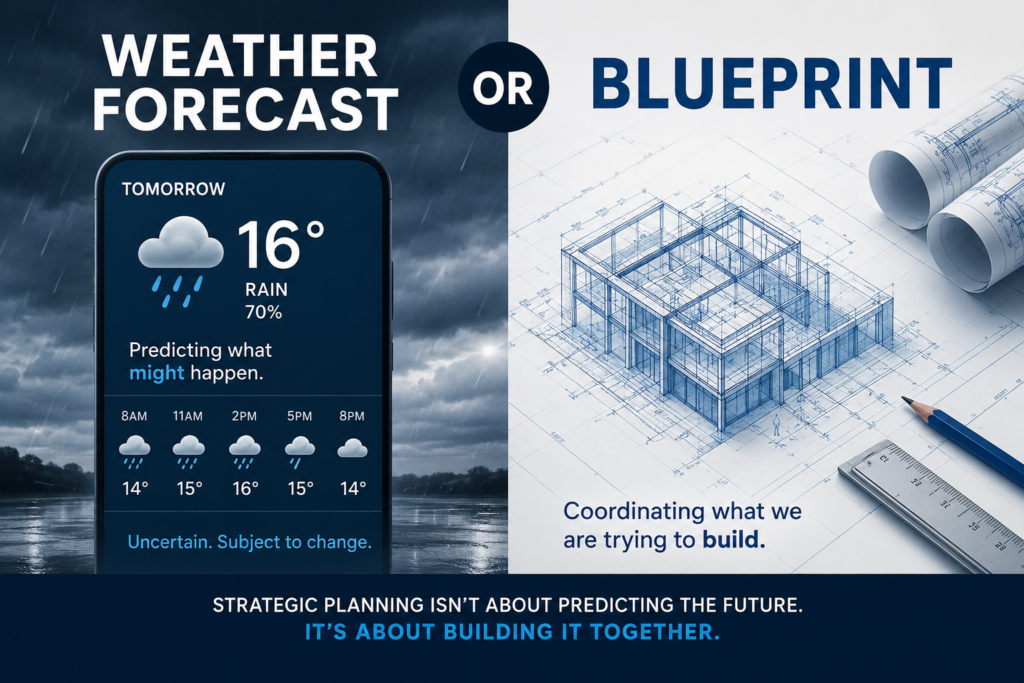

The SSEP: weather forecast or architect’s drawing?

The publications of the past few months expose the tension at the heart of modern strategic energy planning.

One reason this debate becomes confused is that people increasingly talk about the SSEP pathway as though it were a weather forecast. I have heard several conversations over the past few months where someone asks if the SSEP will ultimately prove to be “right” or “wrong”. But that misunderstands the nature of strategic planning.

The SSEP is not really a weather forecast. It is much closer to an architect’s drawing. In fact, NESO has even described it as a blueprint.

A weather forecast attempts to predict what will happen. If tomorrow’s forecast is for rain and the sun comes out instead, it is reasonable to conclude the forecast was wrong.

An architect’s drawing is different. It is not an attempt to predict what builders might independently decide to construct. It is a coordinated instruction for what multiple actors are collectively trying to build. If the final building differs from the drawing, we do not usually conclude that the architect was “wrong”. We are more likely to blame the builder.

There may be good reasons for not following the plan: costs vary, the client could change their mind, the design evolves in response to ground conditions.

The same is true for strategic energy planning.

Strategic planning is not about perfectly predicting the future. It is about choosing a direction, coordinating around it, and adapting intelligently when reality inevitably diverges from the model.

This work was partly developed through conversations with Scottish Renewables in 2025 and 2026. I would like to thank the SR team for their support and review.