I have updated my open-source analysis of Scottish Onshore wind carried out with Regen! This is our second open-source analysis paper in this area and we will do more…

The positive news is that the analysis shows onshore wind farms in north Scotland remain investable in our base case. But this relies on optimistic assumptions about future policy and regulation, particularly locational costs.

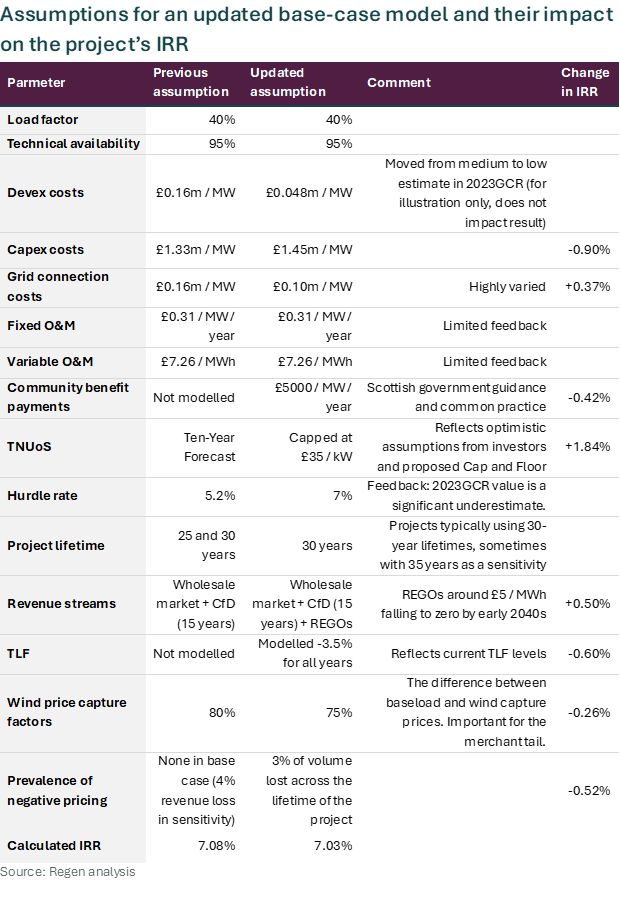

Under our updated base case for a north Scotland wind farm, which uses the AR6 strike price, the Internal Rate of Return (IRR) is 7.03%. According to feedback from the sector this is potentially viable – just – although it is at the bottom of where un-geared hurdle rates are for projects today.

The analysis also shows the precarious position for wind farms in the north which are exposed to the highest locational costs.

This is a particular issue for the 2.6 GW which already has a CfD contract but is yet to reach financial close. Their strike prices are fixed, and they have little wiggle room.

It also has implications for bidding in AR7 where uncertainty over the future could push up strike prices.

To move forward we need sensible decisions on market reform, on locational TNUoS, and on transmission losses to ensure onshore wind can contribute to Clean Power 2030 at the level required.

These insights have been informed by discussions with 25 organisations which have provided detailed feedback on our previous assumptions and identified areas where there are significant differences of opinion across the sector.

See assumptions

Compared with our first paper, important updates include:

- Capital costs have increased

- Hurdle rates are higher

- Developer / investor assumptions about future TNUoS are more optimistic than expected

- Three additional factors are now modelled: locational Transmission Loss Factors (TLFs), Community Benefit Payments, and REGOs.

For me there are three specific areas of concern:

1 – Zonal pricing

Our engagement reinforces the message that revenue reduction and uncertainty under a zonal market are potentially existential without very strong price and volume protection.

2- Locational signals in a national market

There is risk of a divergent assumptions between government and developers about the future of locational TNUoS. Some developers / investors appear to be using optimistic assumptions about TNUoS costs across project lifetimes. But even this year government indicated that they were exploring whether higher locational TNUoS may be required under a reformed national market.

3 – Economic curtailment and negative pricing

Understanding is patchy across the sector and needs to be improved. I am concerned that under a Clean Power 2030 world the impact could be significant. But, as yet, there is no consensus.