“We need a clearer understanding of the drivers and potential scale of economic curtailment to inform the reformed national pricing process and future renewable support mechanisms.”

As part of today’s reformed national pricing process, there is an acute focus on reducing network curtailment, the renewable generation we have to switch off due to grid constraints, and the cost of replacing it with non-renewable generation elsewhere.

In this working paper, I look at a different type of curtailment: oversupply of renewables, when the output of wind and solar exceeds what the market can use, even after accounting for flexibility.

This is economic curtailment: curtailment driven by the national balance of supply and demand, not by network limits.

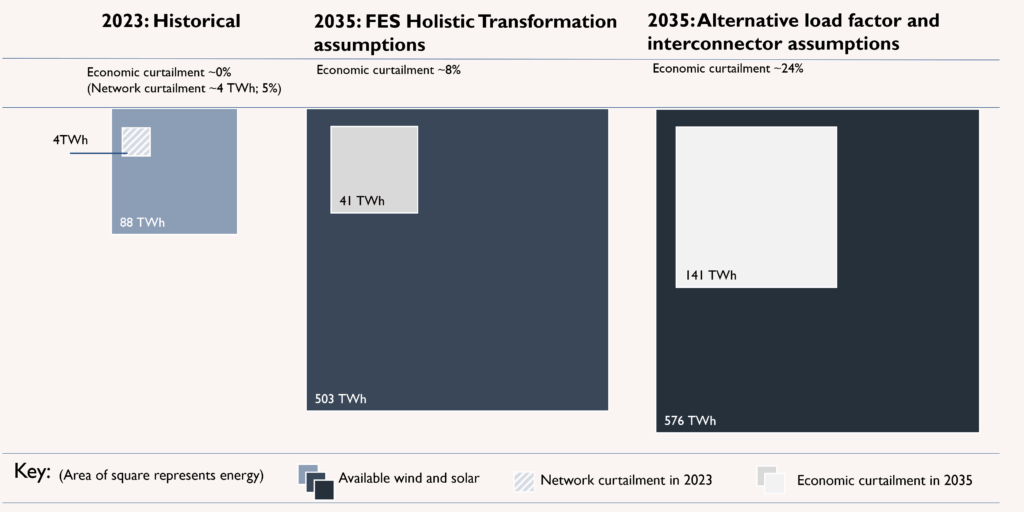

One of the key messages of the paper is that economic curtailment could be far larger than today’s network curtailment, but its potential scale is still poorly understood. NESO’s FES 2025 modelling for the Holistic Transformation scenario suggests 41 TWh of economic curtailment in 2035. For comparison that is 10 times the volume of network curtailment in 2023.

However, NESO appears to use relatively low load factor assumptions for renewables and relatively optimistic assumptions for interconnector exports. The volume of economic curtailment is sensitive to these assumptions, and tweaking them – as I have done in modelling for this paper – suggests that the volume could be significantly higher: as much as 141 TWh.

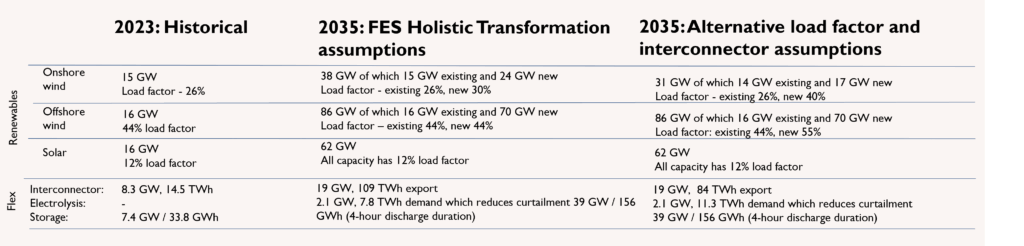

Assumptions:

I don’t claim this is the ‘right’ answer, rather the analysis shows that the assumptions used can make a big difference. As a sector, we haven’t yet started to explore these issues in detail.

As well as exploring the overall volume, the paper begins to explore how economic curtailment will be spread across the fleet. Importantly, and unlike network curtailment, this is not a centralised process, and its distribution is not set by NESO. Instead, it is a natural part of energy trading and is allocated by the wholesale energy market.

Impacts

The paper also considered the impact of economic curtailment. There are three types: generator, market / system, and consumer impacts.

Generator impacts: include a direct loss of revenue and unlike network curtailment, there is no mechanism to compensate generators. There is also significant uncertainty over the future level of economic curtailment, something that will introduce risk for investors.

Market impacts: include how economic curtailment interacts with the current CfD model to create distortions in the wholesale market. For example, the current pay-on-output CfD model means generators with pre-AR4 generators are likely to offer their generation at a negative price where their CfD will more than cover this payment. At the same time the negative pricing rule introduced in AR4, under which CfD uplift payments are not made when the day-ahead wholesale price goes negative, means that more recent generators may be incentivised to bid at exactly zero (although various other factors such as gaming, market power etc. may adjust the optimal behaviour)

Consumer impacts: arise as a consequence of the first two categories. Lower revenue and higher risk for generators could push higher clearing prices in CfD auctions, increasing support payments which come directly from bills. And distortions in the wholesale market is likely to reduce its effectiveness in allocating generation and flexibility efficiently.

Recommendations and next steps

The paper includes a series of recommendations for government and the sector. These focus on the need to understand these issues more clearly:

1. Understand the scale of economic curtailment

Commission analysis to assess curtailment levels across a range of scenarios and assumptions.

Quantify the financial impact on generators and the implications for investability and CfD strike price bids.

Quantify the risk that uncertainty about the level and distribution of economic curtailment creates for market participants, including CfD holders. Conduct technology-specific analysis for both wind and solar.

2. Design markets and systems to manage it

Ensure the RNP process addresses the question of how economic curtailment is allocated by the market.

Review tie-breaker rules in power exchange auctions.

Assess the likely impact on merchant generators and prevent curtailment from driving premature closure.

Explore economic curtailment through a locational lens, considering its interaction with network curtailment.

Integrate a growing understanding of economic curtailment into strategic spatial energy and network planning.

3. Review the implications for CfD design

Assess how current CfD rules distort market behaviour during periods of economic curtailment and quantify the detriment created.

Quantify the likely level of negative pricing in the market under a range of assumptions about trading behaviour.

Quantify how rising economic curtailment increases risk for market participants and consumers.

Consider CfD reforms that reduce or remove market distortions. This should include options that move away from ‘pay-on-output’ support such as deemed or capacity-based CfDs.

4. Treat economic curtailment as an opportunity

Use evidence on the scale of curtailment to identify opportunities for flexibility and accelerated electrification of heat, transport, industry and green hydrogen.

Embed these opportunities in policy and regulatory frameworks – for example, the Hydrogen Production Business Model.

As understanding of economic curtailment grows, ensure markets and support mechanisms enable long-term investment in demand and flexibility, as well as short-term dispatch.