A £25/ MWh locational difference in transmission charges for wind by the early 2030s?

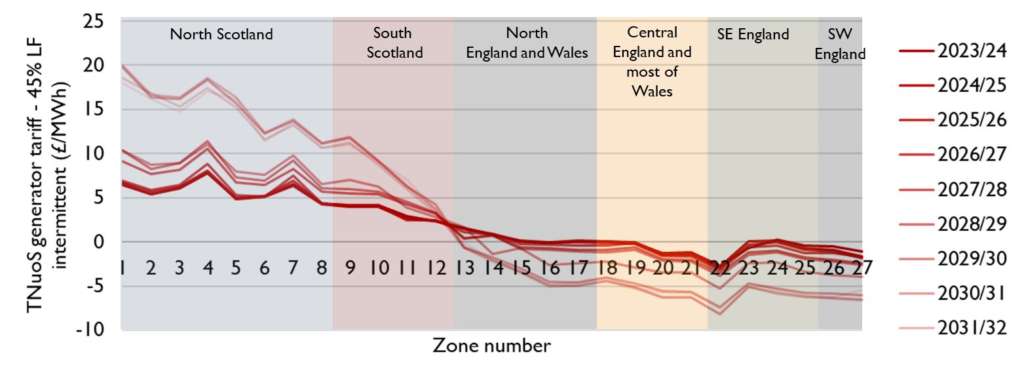

National Grid ESO published ten year TNUoS forecasts this week giving an illustration of what transmission charges would look like under the current methodology out to 2034. Although the values are published in pounds per kilowatt of installed capacity I often find it useful to think about them on a pounds per megawatt-hour basis as it allows comparison with estimates of the levelised cost of energy.

Here are some different ways to look at the numbers in the forecast:

On a capacity basis:

🔹 A 1 GW offshore wind farm in North Scotland would, in 2034, be paying £71m per year compared with £26m today.

🔹 By comparison the same sized wind farm connecting into Pembrokeshire (such as floating wind capacity in the Celtic Sea) would *be paid* £23m per year compared with £5m today.

On an energy basis:

🔹 Charges for wind in North Scotland would equate to £17.91/MWh in 2032 compared with £6.45/MWh today. For comparison that is around 41% of the estimated Levelised Cost of Energy from wind according to the most recent UK Government Generation Cost Report.

🔹 The negative charges in the south accentuate the locational signal further – the difference between Pembrokeshire and North Scotland is £23.67 / MWh more than 50% of the LCoE for wind.

🔹 The numbers are actually slightly bigger for 2030-32 where the Pembrokeshire to north Scotland difference exceeds £25 / MWh.

The increasing difference between charges across the country is driven by substantial transmission investment planned over the coming decade. There is a step change in the graph at 2030, the year in which reinforcements planned under HND and greenlit through Ofgem’s ASTI framework.

TNUoS, therefore, delivers a very strong locational signal for generation developers (something that Regen picked up on in a recent locational signals paper). These new forecasts pose a number of questions:

🔸 is the strength of the locational signal really cost reflective in terms of the transmission investment that generation drives? And does it actually drive behaviour?

🔸 Rather than nudge generation development further south, will the size of TNUoS and the locational difference act as a barrier to development?

🔸 How do we appropriately balance the size of locational signal with the challenge of delivering net zero electricity by 2035 and other societal outcomes?

The difference seems very large to me. I picked north Scotland and Pembrokeshire as two locations where we could be connecting substantial wind next decade through including thorough hashtag#Scotwind and hashtag#CelticSea leasing rounds. Whilst locational signals are important, as the debate around hashtag#REMA shows, it is also clear that we need more-or-less all the feasible renewable capacity we can build in the next decade if we are to deliver on societal aims of low carbon, cheap generation and stable prices; all outcomes that wind generation can help deliver.